Basel, CH – December 2022

Disassembly with Meat and Fish Management 2/4

In addition to their other applications as Execution and Planning, cut lists are used in Disassembly Costing processes. These processes are aimed at planning, managing and analyzing the costs arising in the production processes. Effectively, the cut list serves as a multilevel inverse BOM and acts in a similar manner as BOMs and routings in the assembly scenarios supported by SAP standard costing.

Disassembly Calculations

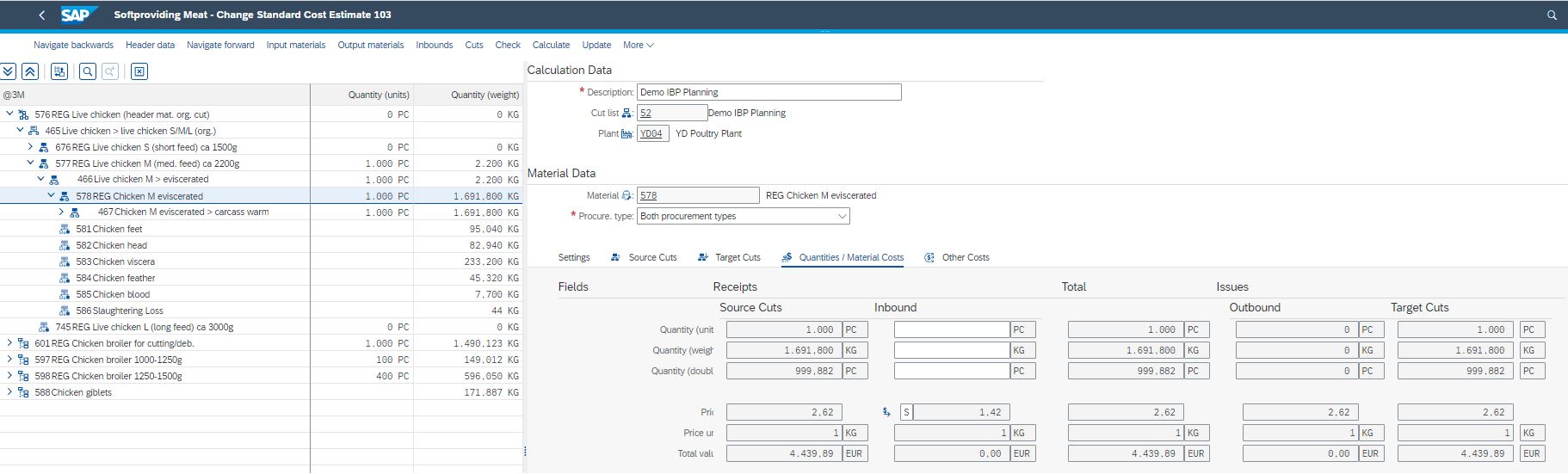

Disassembly calculations distribute the quantities and material costs from inputs to the outputs following the hierarchy of the cuts while taking into account the cut list structure and other costs (labor and machine) occurring at each cut list level:

- Quantities of each output are determined by hierarchically distributing the quantities of the input materials (usually live animals and primal cuts) to the outputs in accordance with output percentages.

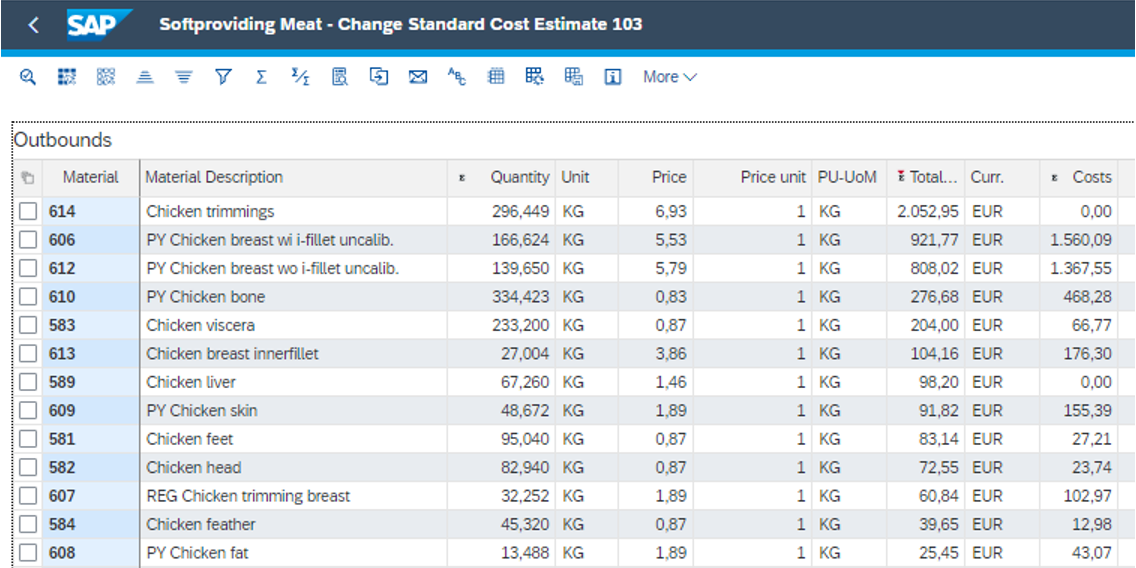

- Material costs of cut list inputs (usually live animals and primal cuts) are hierarchically distributed to the outputs in accordance with output percentages, material cost equivalences, as well as fixed price indicators and values.

- If a routing is assigned to a cut, the quantities and values of other costs (labor and machine costs originated from the assigned routing) are determined based on the calculated input quantity of the cut and are distributed to the cut outputs in accordance with output percentages, material cost equivalences, and fixed prices. If an output material acts as the input in a subsequent cut, other costs assigned to this material are added to inbound other costs of the subsequent cut and distributed to the outputs of the following cut together with the subsequent cut’s own other costs.

Fixed Prices, Equivalences, Price and Equivalence Sources

Equivalences and fixed prices are used in material and other costs distribution in combination with output weight percentages.

First, the inbound value is determined for material costs or other costs of the current cut. Then, the value of each fixed-price output is calculated by multiplying their prices with the calculated quantity and subtracted from the inbound quantity. Finally, the remaining value is distributed to the materials without fixed prices.

The factors for value distribution to the outputs without fixed prices are defined by multiplying the output weight percentage with the respective equivalence for each output.

Sources of fixed price indicators, fixed prices, and equivalences facilitate and optimize master data management. This means that the master data can be stored both in the material master (plant-specific/cross-plant) and in the cut (specific to a cut in which the material occurs).

Calculation example

- Inbound weight: 2,200 KG

- Inbound value: 4,840 EUR

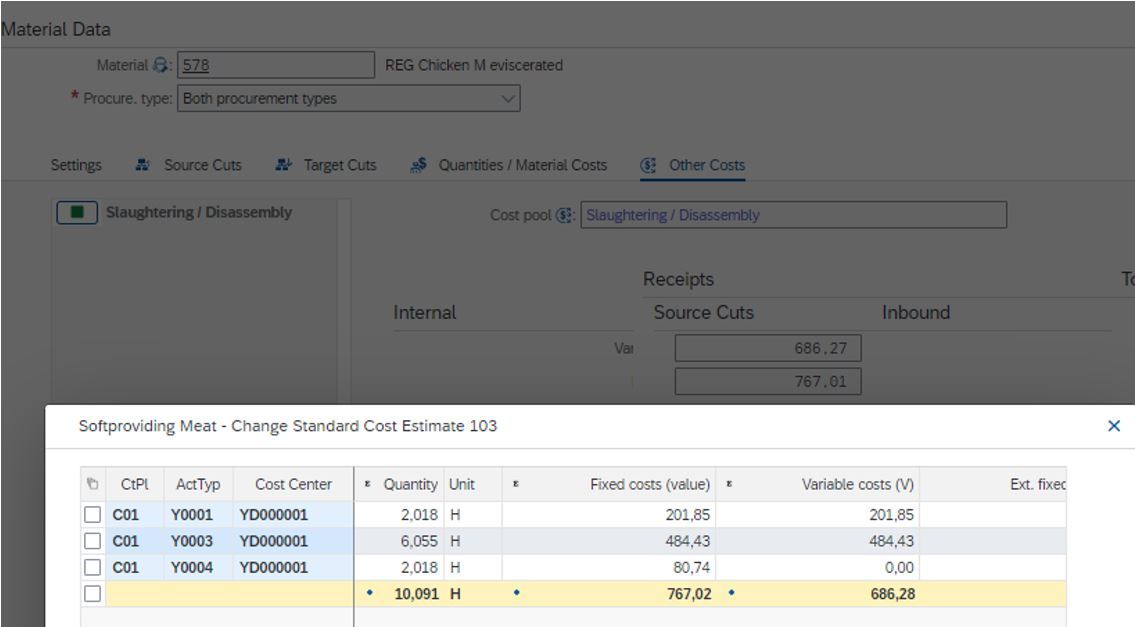

Cost Pools

Cost pools can be used to differentiate between different groups of activity types used in the routings assigned to the cuts. Each cost pool has its own set of fixed prices and equivalences for other costs. For example, it is possible to configure different distribution logic for material and labor costs in each cut.

Standard Cost Estimate

Standard cost estimate functionality allows you to calculate the standard prices of all outputs in a current cut list. The Push calculation type is used for standard cost estimates (details on calculation types are described in this text).

The result of the standard cost estimate is a calculation without quantity structure in S/4 created for each relevant output of the cut list. These calculations without quantity structure can be later used for the cost estimate calculation of packed meat and further processed materials.

Typically, a standard cost estimate is following these three steps in cases where the Disassembly module is used:

- SAP standard costing run for live animals (if applicable)

- Disassembly standard cost estimate calculation

- SAP standard costing run for packed meat and further processed materials

Actual Calculation in a Disassembly Order

During disassembly execution, input and output quantities are recorded. When both inputs and outputs are available for a disassembly order, a calculation is performed based on the registered quantities. In contrast to disassembly costing, the actual calculation is push-pull, that is, balancing of input and output quantities is effectuated.

Similar to standard disassembly costing, material costs of input materials are distributed to the output materials and other costs are added to the cuts wherever relevant and distributed down the hierarchy. As a result, material and other costs are determined for each output material with actual quantity recorded. While the material movements are typically valued with standard prices, the actual calculation data serve as a background in the following processes:

- The sum of material costs and other costs can be entered as the equivalence in the order settlement rule for a given material. These equivalence rules are used in the preliminary settlement of the costs aggregated on the disassembly order to the order items corresponding to the output materials

- Input quantities defined for each cut in the calculation can be used to automatically confirm all order operations using the activity quantities calculated proportionally to the cut input quantities.

Integration with Material Ledger

Material and other costs in actual calculations are aggregated for all disassembly orders in the period being closed and passed to the Material Ledger. These values are later used to distribute the variances in Disassembly and the preceding production processes to disassembly outputs in accordance with actual production results.

If this article has piqued your interest, please do not hesitate to contact Stephan Kronbichler (Business Development) for further information: E-mail, phone +41 (0)61 508 21 42.